Start date cannot be after end date.

Contact Non-Squeezing in Various Closed Prequantizations

Presenter

- Pierre-Alexandre Arlove

February 21, 2025

IAS

José Alejandro Samper Casas - The cd-index of a semi-Eulerian complex - IPAM at UCLA

Presenter

- José Samper Casas

February 14, 2025

IPAM

The Spectral Diameter of a Liouville Domains and its Applications

Presenter

- Pierre-Alexandre Mailhot

October 28, 2022

IAS

Ensemble-Average Representation of Pt clusters in Conditions of Catalysis, accessed through GPU Accelerated Deep Neural Network Fitting Global Optimization

Presenter

- Anastassia Alexandrova

November 18, 2016

IPAM

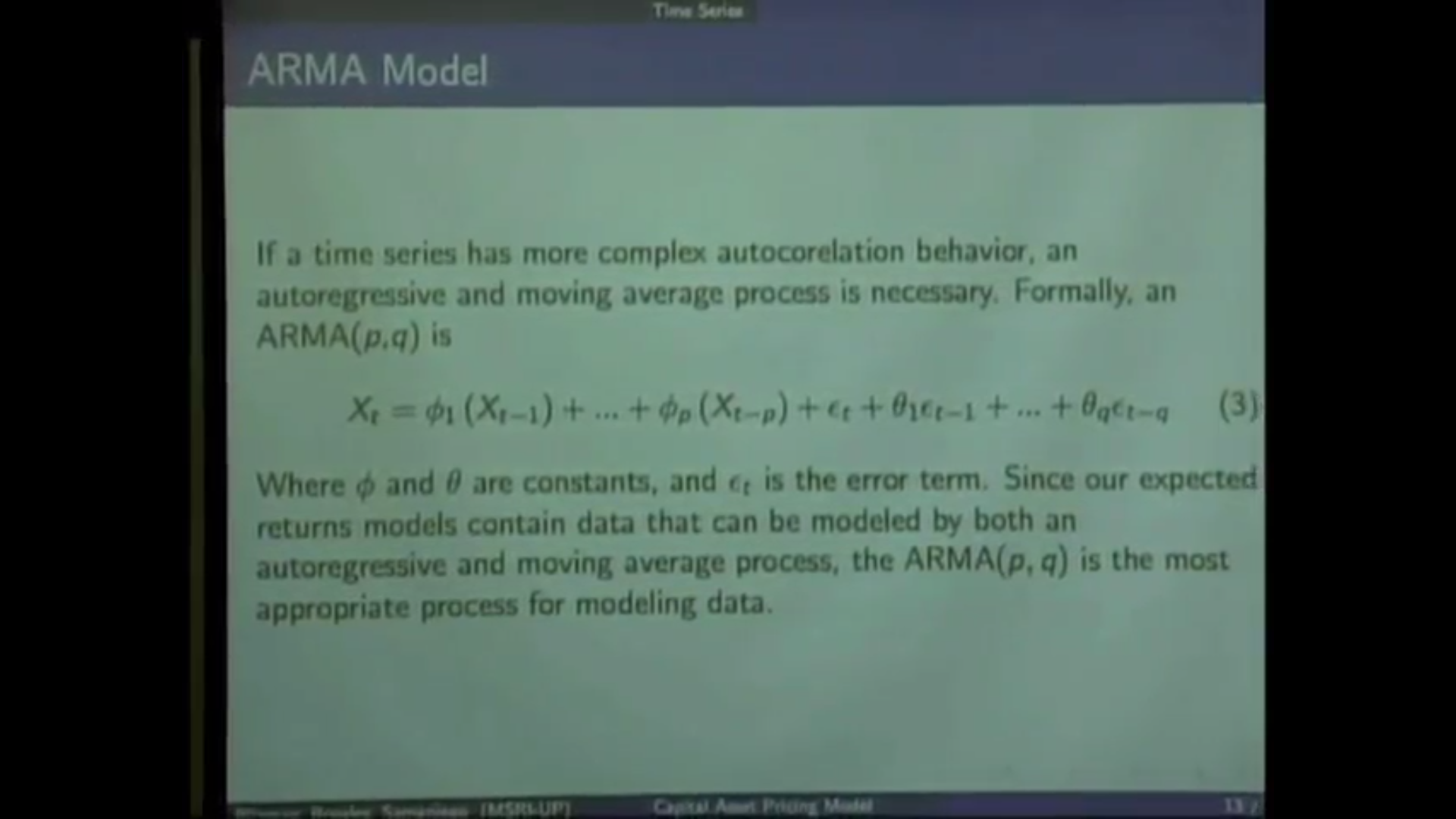

MSRI-UP 2011: Mathematical Finance, presentation 5: Conditioning the Capital Asset Pricing Model (CAPM) with Implied Volatility

Presenters

- Allyson Blizman

- Elisa Rosales

- Alejandro Samaniego

July 22, 2011

SLMath

Panel Session: "Uncertainty in PDEs and optimizations, interations, synergies, challenges" <br>Moderator: <b>Suvrajeet Sen</b> (Ohio State University)

Presenters

- Timothy Barth

- Omar Ghattas

- Alejandro Jofre

- Robert Lipton

- Stephen Robinson

October 20, 2010

IMA

Factorizations, centers, and the Jucys—Murphy elements of the Hecke algebra

Presenter

- Sarah Brauner

September 18, 2025

ICERM